### Describe Your Changes

* `sort` param is unused by the current website engine, and was present only for compatibility

with previous website engine. It is time to remove it as it makes no effect

* re-structure guides content into folders to simplify assets management

### Checklist

The following checks are **mandatory**:

- [ ] My change adheres [VictoriaMetrics contributing

guidelines](https://docs.victoriametrics.com/contributing/).

(cherry picked from commit 35d77a3bed)

57 KiB

| title | weight | menu | aliases | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Models | 1 |

|

|

This section describes Models component of VictoriaMetrics Anomaly Detection (or simply vmanomaly) and the guide of how to define a respective section of a config to launch the service.

vmanomalyincludes various built-in models.- you can also integrate your custom model - see custom model.

Note: Starting from v1.10.0 model section in config supports multiple models via aliasing.

Also,vmanomalyexpects model section to be namedmodels. Using old (flat) format withmodelkey is deprecated and will be removed in future versions. Havingmodelandmodelssections simultaneously in a config will result in onlymodelsbeing used:

models:

model_univariate_1:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 2.5

queries: ['query_alias2'] # referencing queries defined in `reader` section

model_multivariate_1:

class: 'isolation_forest_multivariate' # or model.isolation_forest.IsolationForestMultivariateModel until v1.13.0

contamination: 'auto'

args:

n_estimators: 100

# i.e. to assure reproducibility of produced results each time model is fit on the same input

random_state: 42

# if there is no explicit `queries` arg, then the model will be run on ALL queries found in reader section

# ...

Old-style configs (< 1.10.0)

model:

class: "zscore" # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3.0

# no explicit `queries` arg is provided

# ...

will be implicitly converted to

models:

default_model: # default model alias, backward compatibility

class: "model.zscore.ZscoreModel"

z_threshold: 3.0

# queries arg is created and propagated with all query aliases found in `queries` arg of `reader` section

queries: ['q1', 'q2', 'q3'] # i.e., if your `queries` in `reader` section has exactly q1, q2, q3 aliases

# ...

Common args

From 1.10.0, common args, supported by every model (and model type) were introduced.

Queries

Introduced in 1.10.0, as a part to support multi-model configs, queries arg is meant to define queries from VmReader particular model should be run on (meaning, all the series returned by each of these queries will be used in such model for fitting and inferencing).

queries arg is supported for all the built-in (as well as for custom) models.

This arg is backward compatible - if there is no explicit queries arg, then the model, defined in a config, will be run on ALL queries found in reader section:

models:

model_alias_1:

# ...

# no explicit `queries` arg is provided

will be implicitly converted to

models:

model_alias_1:

# ...

# if not set, `queries` arg is created and propagated with all query aliases found in `queries` arg of `reader` section

queries: ['q1', 'q2', 'q3'] # i.e., if your `queries` in `reader` section has exactly q1, q2, q3 aliases

Schedulers

Introduced in 1.11.0, as a part to support multi-scheduler configs, schedulers arg is meant to define schedulers particular model should be attached to.

schedulers arg is supported for all the built-in (as well as for custom) models.

This arg is backward compatible - if there is no explicit schedulers arg, then the model, defined in a config, will be attached to ALL the schedulers found in scheduler section:

models:

model_alias_1:

# ...

# no explicit `schedulers` arg is provided

will be implicitly converted to

models:

model_alias_1:

# ...

# if not set, `schedulers` arg is created and propagated with all scheduler aliases found in `schedulers` section

schedulers: ['s1', 's2', 's3'] # i.e., if your `schedulers` section has exactly s1, s2, s3 aliases

Provide series

Introduced in 1.12.0, provide_series arg limit the output generated by vmanomaly for writing. I.e. if the model produces default output series ['anomaly_score', 'yhat', 'yhat_lower', 'yhat_upper'] by specifying provide_series section as below, you limit the data being written to only ['anomaly_score'] for each metric received as a subject to anomaly detection.

models:

model_alias_1:

# ...

provide_series: ['anomaly_score'] # only `anomaly_score` metric will be available for writing back to the database

Note If provide_series is not specified in model config, the model will produce its default model-dependent output. The output can't be less than ['anomaly_score']. Even if timestamp column is omitted, it will be implicitly added to provide_series list, as it's required for metrics to be properly written.

Detection direction

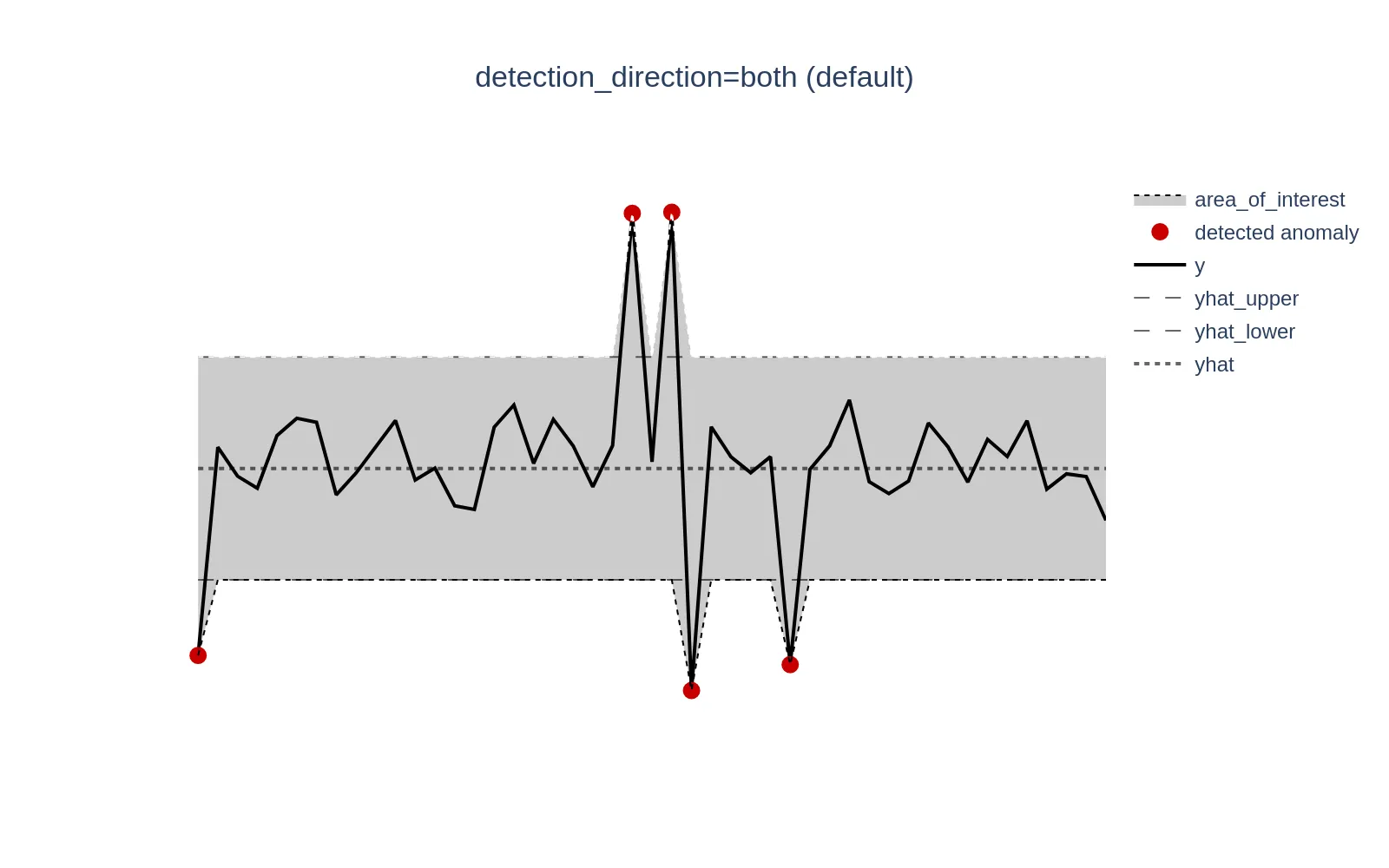

Introduced in 1.13.0, detection_direction arg can help in reducing the number of false positives and increasing the accuracy, when domain knowledge suggest to identify anomalies occurring when actual values (y) are above, below, or in both directions relative to the expected values (yhat). Available choices are: both, above_expected, below_expected.

Here's how default (backward-compatible) behavior looks like - anomalies will be tracked in both directions (y > yhat or y < yhat). This is useful when there is no domain expertise to filter the required direction.

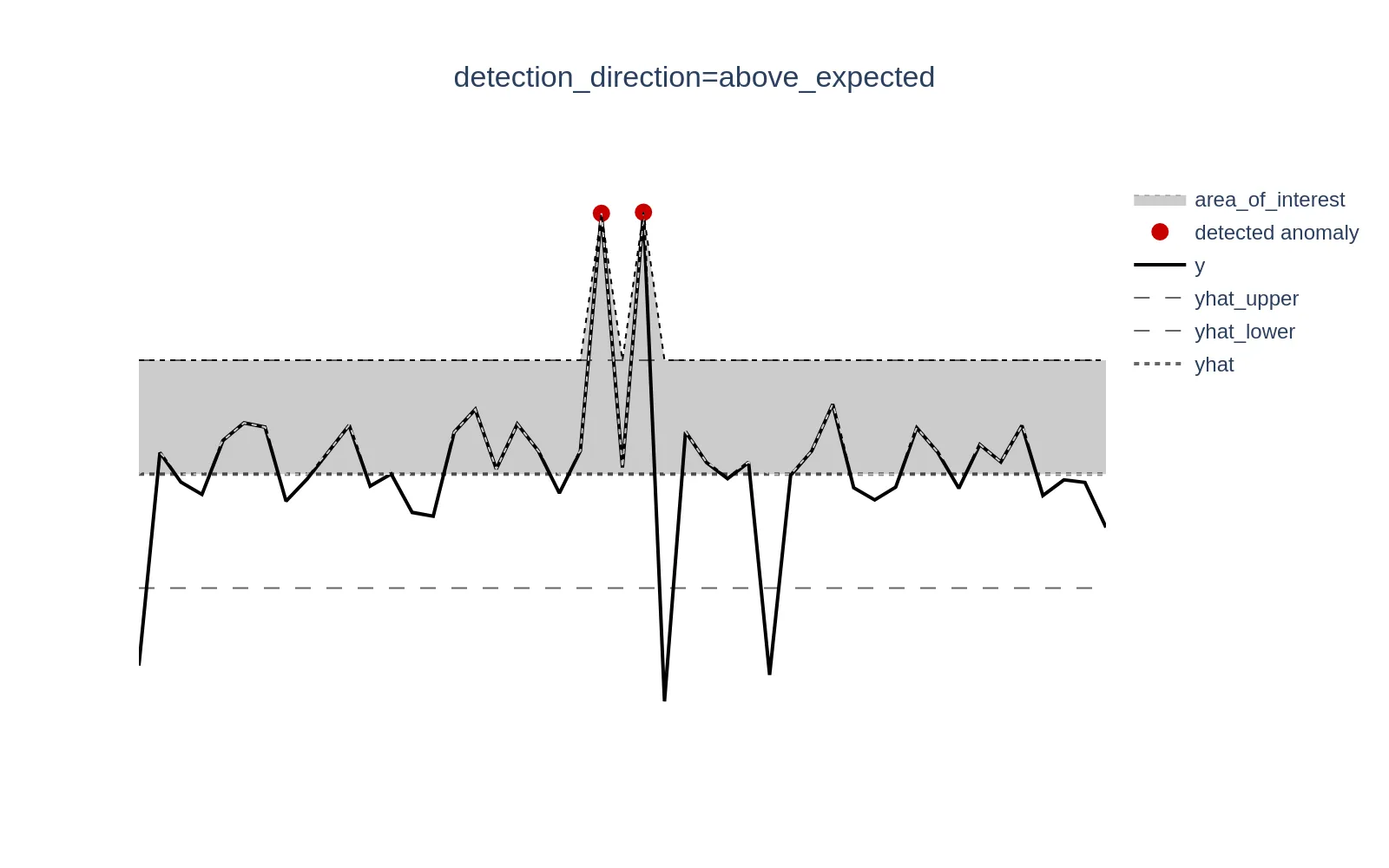

When set to above_expected, anomalies are tracked only when y > yhat.

Example metrics: Error rate, response time, page load time, number of failed transactions - metrics where lower values are better, so higher values are typically tracked.

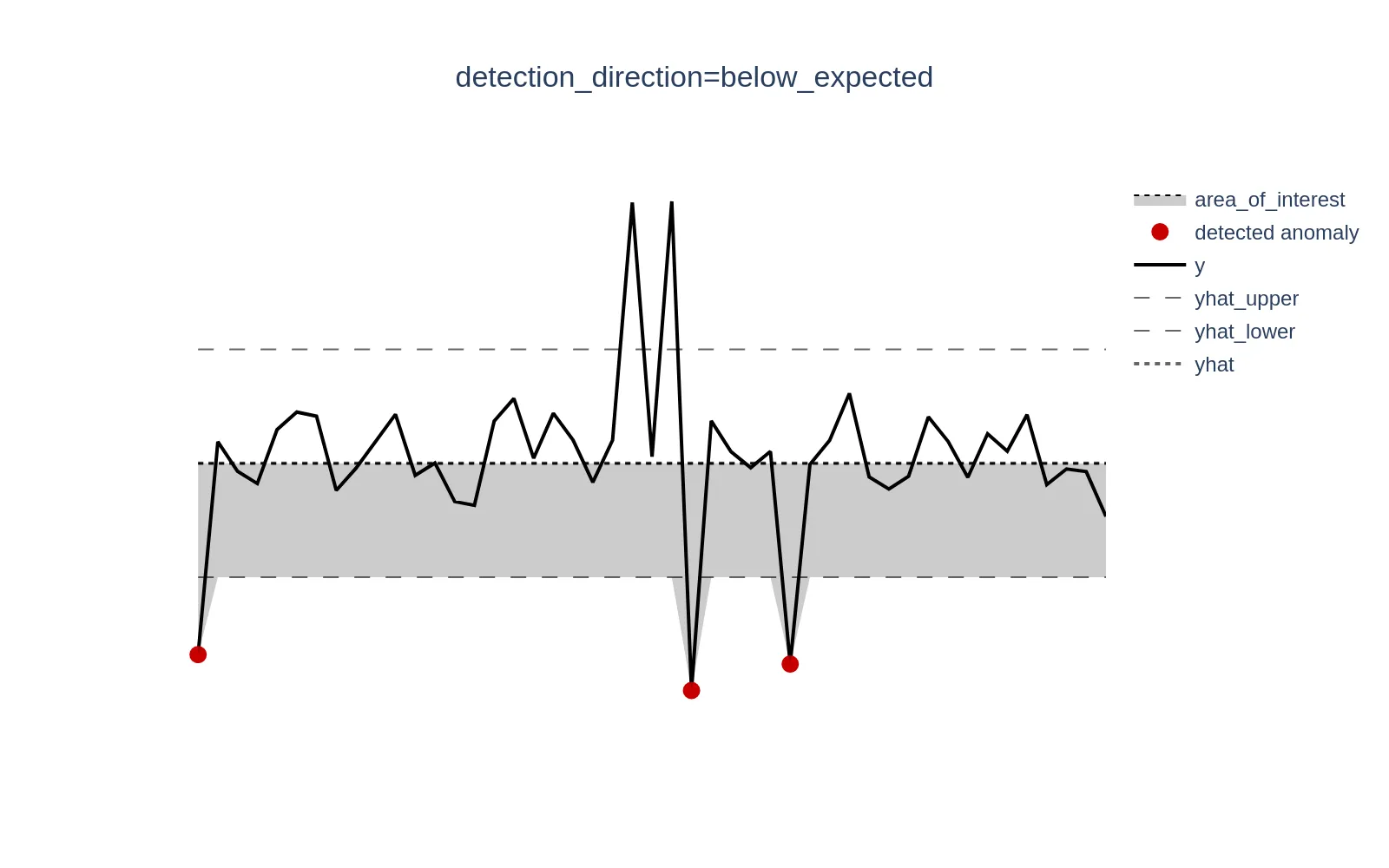

When set to below_expected, anomalies are tracked only when y < yhat.

Example metrics: Service Level Agreement (SLA) compliance, conversion rate, Customer Satisfaction Score (CSAT) - metrics where higher values are better, so lower values are typically tracked.

Config with a split example:

models:

model_above_expected:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3.0

# track only cases when y > yhat, otherwise anomaly_score would be explicitly set to 0

detection_direction: 'above_expected'

# for this query we do not need to track lower values, thus, set anomaly detection tracking for y > yhat (above_expected)

queries: ['query_values_the_lower_the_better']

model_below_expected:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3.0

# track only cases when y < yhat, otherwise anomaly_score would be explicitly set to 0

detection_direction: 'below_expected'

# for this query we do not need to track higher values, thus, set anomaly detection tracking for y < yhat (above_expected)

queries: ['query_values_the_higher_the_better']

model_bidirectional_default:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3.0

# track in both direction, same backward-compatible behavior in case this arg is missing

detection_direction: 'both'

# for this query both directions can be equally important for anomaly detection, thus, setting it bidirectional (both)

queries: ['query_values_both_direction_matters']

reader:

# ...

queries:

query_values_the_lower_the_better: metricsql_expression1

query_values_the_higher_the_better: metricsql_expression2

query_values_both_direction_matters: metricsql_expression3

# other components like writer, schedule, monitoring

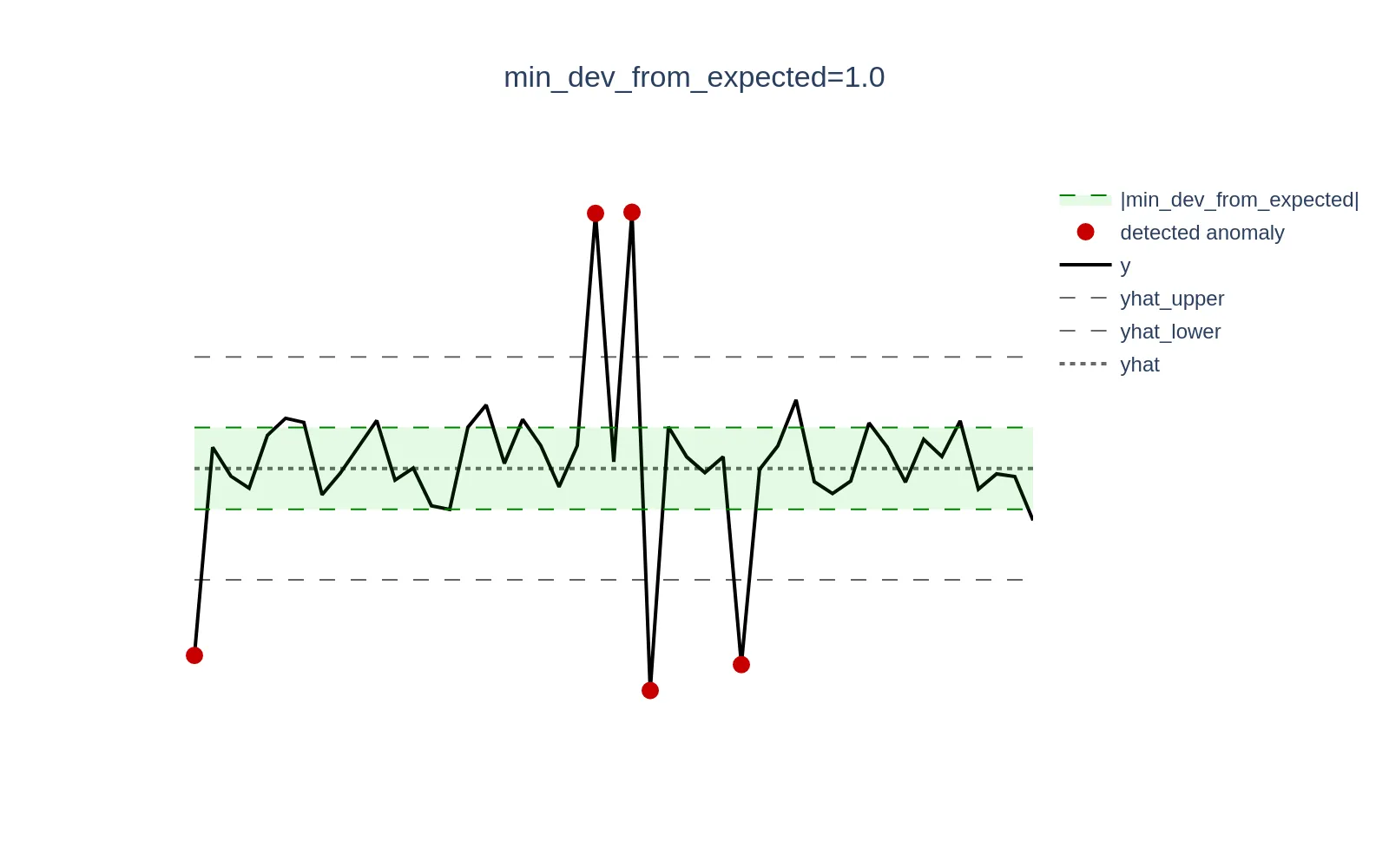

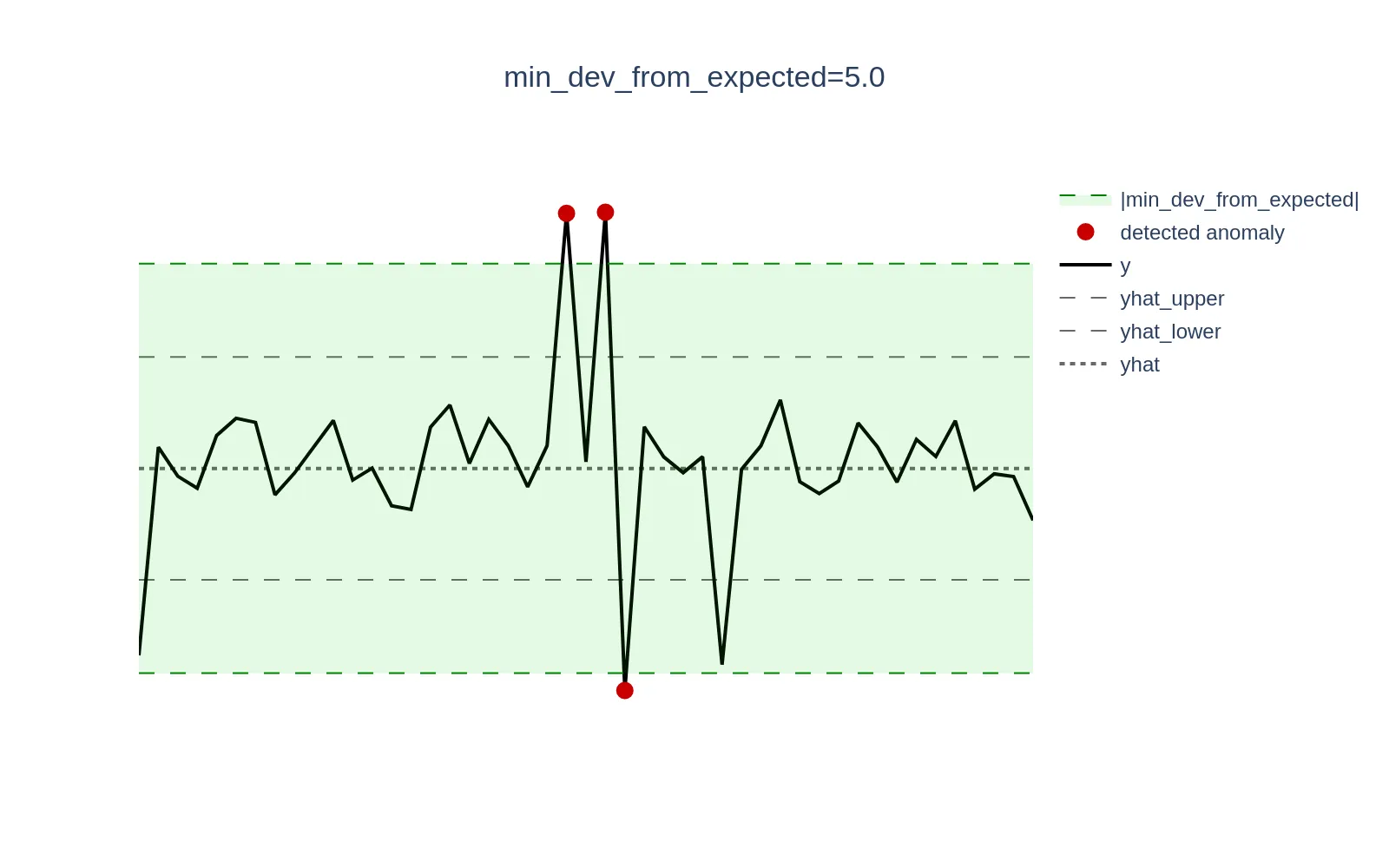

Minimal deviation from expected

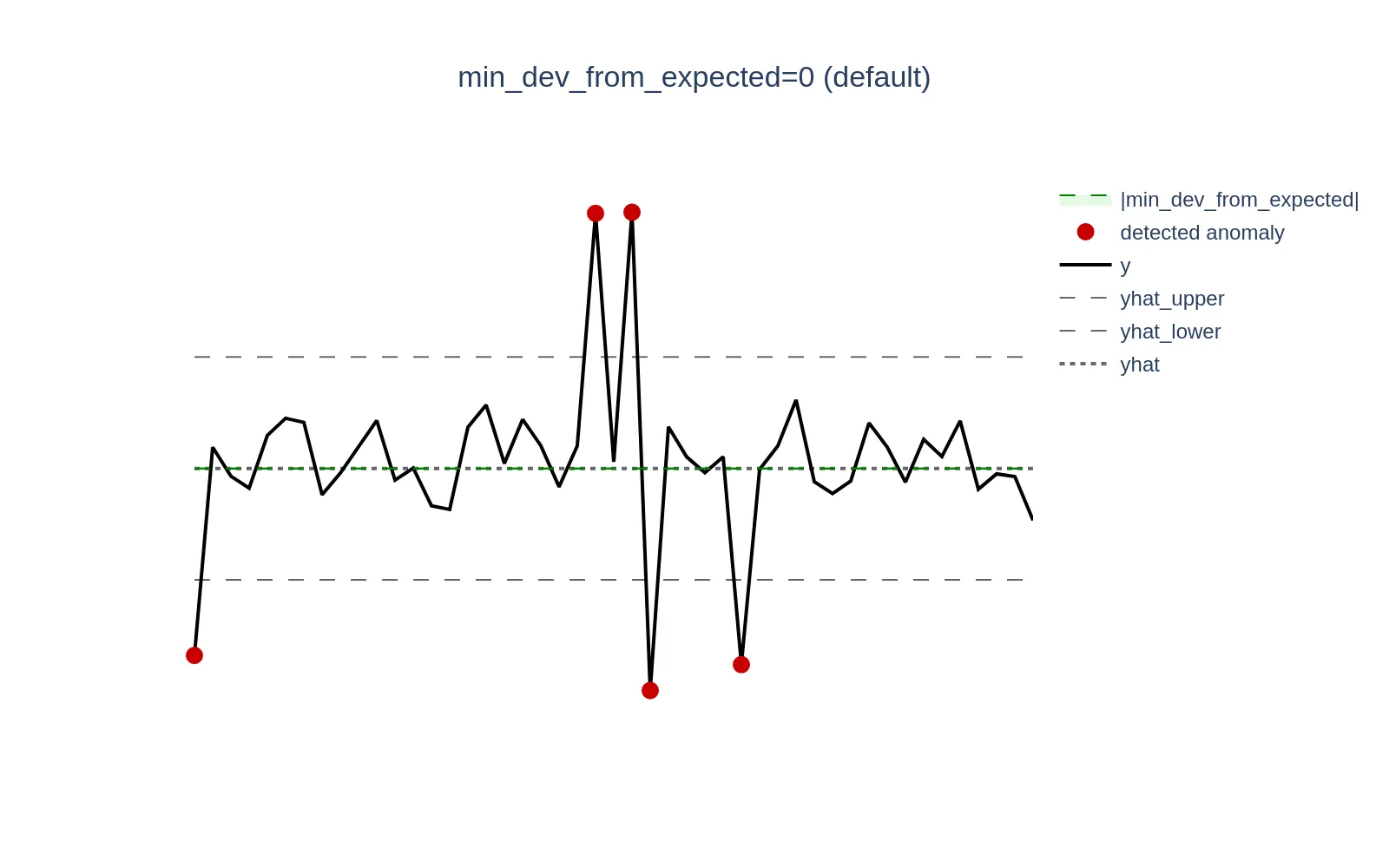

Introduced in v1.13.0, the min_dev_from_expected argument is designed to reduce false positives in scenarios where deviations between the actual value (y) and the expected value (yhat) are relatively high. Such deviations can cause models to generate high anomaly scores. However, these deviations may not be significant enough in absolute values from a business perspective to be considered anomalies. This parameter ensures that anomaly scores for data points where |y - yhat| < min_dev_from_expected are explicitly set to 0. By default, if this parameter is not set, it behaves as min_dev_from_expected=0 to maintain backward compatibility.

Note

:

min_dev_from_expectedmust be >= 0. The higher the value ofmin_dev_from_expected, the fewer data points will be available for anomaly detection, and vice versa.

Example: Consider a scenario where CPU utilization is low and oscillates around 0.3% (0.003). A sudden spike to 1.3% (0.013) represents a +333% increase in relative terms, but only a +1 percentage point (0.01) increase in absolute terms, which may be negligible and not warrant an alert. Setting the min_dev_from_expected argument to 0.01 (1%) will ensure that all anomaly scores for deviations <= 0.01 are set to 0.

Visualizations below demonstrate this concept; the green zone defined as the [yhat - min_dev_from_expected, yhat + min_dev_from_expected] range excludes actual data points (y) from generating anomaly scores if they fall within that range.

Example config of how to use this param based on query results:

# other components like writer, schedulers, monitoring ...

reader:

# ...

queries:

# the usage of min_dev should reduce false positives here

need_to_include_min_dev: small_abs_values_metricsql_expression

# min_dev is not really needed here

normal_behavior: no_need_to_exclude_small_deviations_metricsql_expression

models:

zscore_with_min_dev:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3

min_dev_from_expected: 5.0

queries: ['need_to_include_min_dev'] # use such models on queries where domain experience confirm usefulness

zscore_wo_min_dev:

class: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3

# if not set, equals to setting min_dev_from_expected == 0

queries: ['normal_behavior'] # use the default where it's not needed

Model types

There are 2 model types, supported in vmanomaly, resulting in 4 possible combinations:

Each of these models can be of type

Moreover, starting from v1.15.0, there exist online (incremental) models subclass. Please refer to the correspondent section for more details.

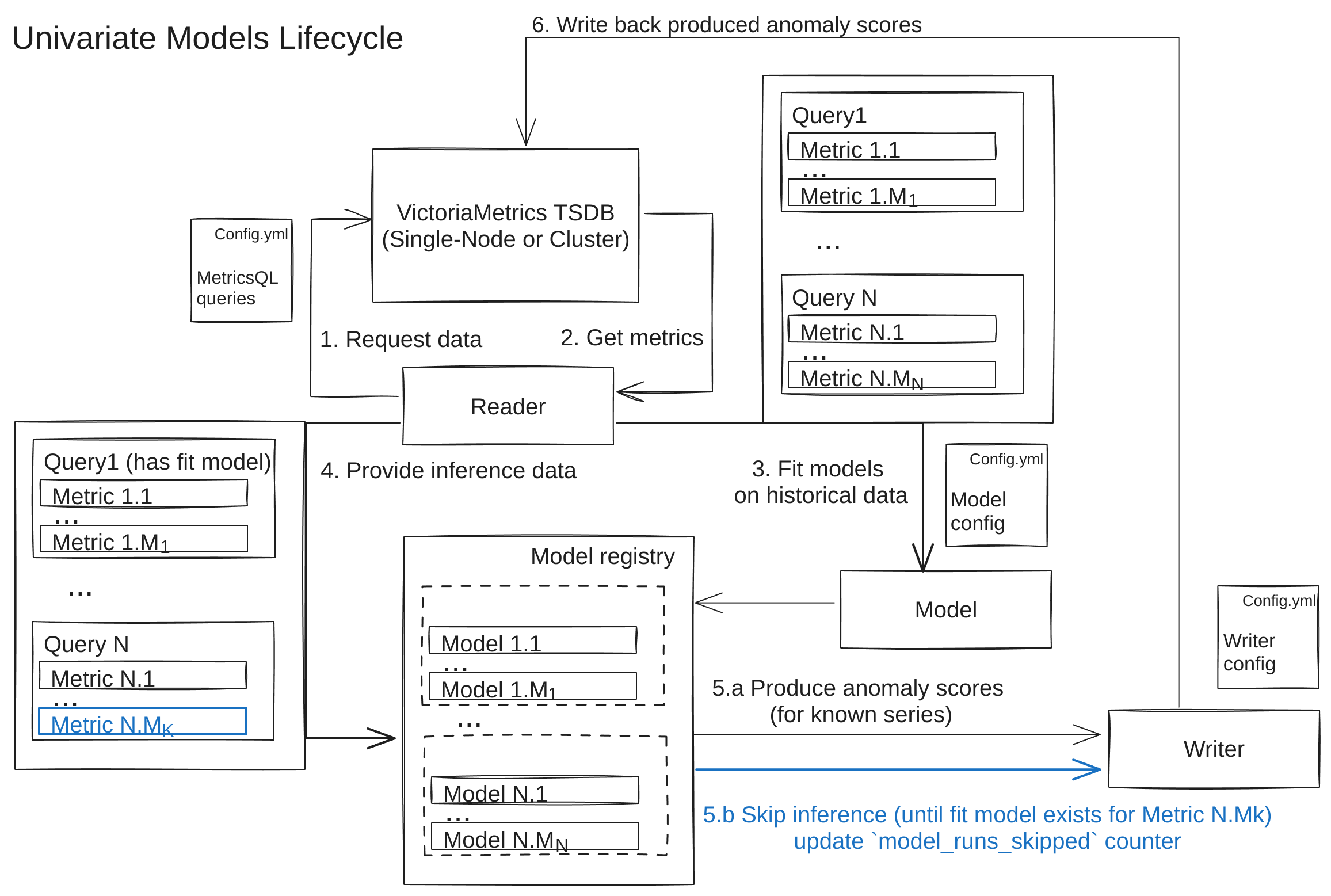

Univariate Models

For a univariate type, one separate model is fit/used for inference per each time series, defined in its queries arg.

For example, if you have some univariate model, defined to use 3 MetricQL queries, each returning 5 time series, there will be 3*5=15 models created in total. Each such model produce individual output for each of time series.

If during an inference, you got a series having new labelset (not present in any of fitted models), the inference will be skipped until you get a model, trained particularly for such labelset during forthcoming re-fit step.

Implications: Univariate models are a go-to default, when your queries returns changing amount of individual time series of different magnitude, trend or seasonality, so you won't be mixing incompatible data with different behavior within a single fit model (context isolation).

Examples: Prophet, Holt-Winters

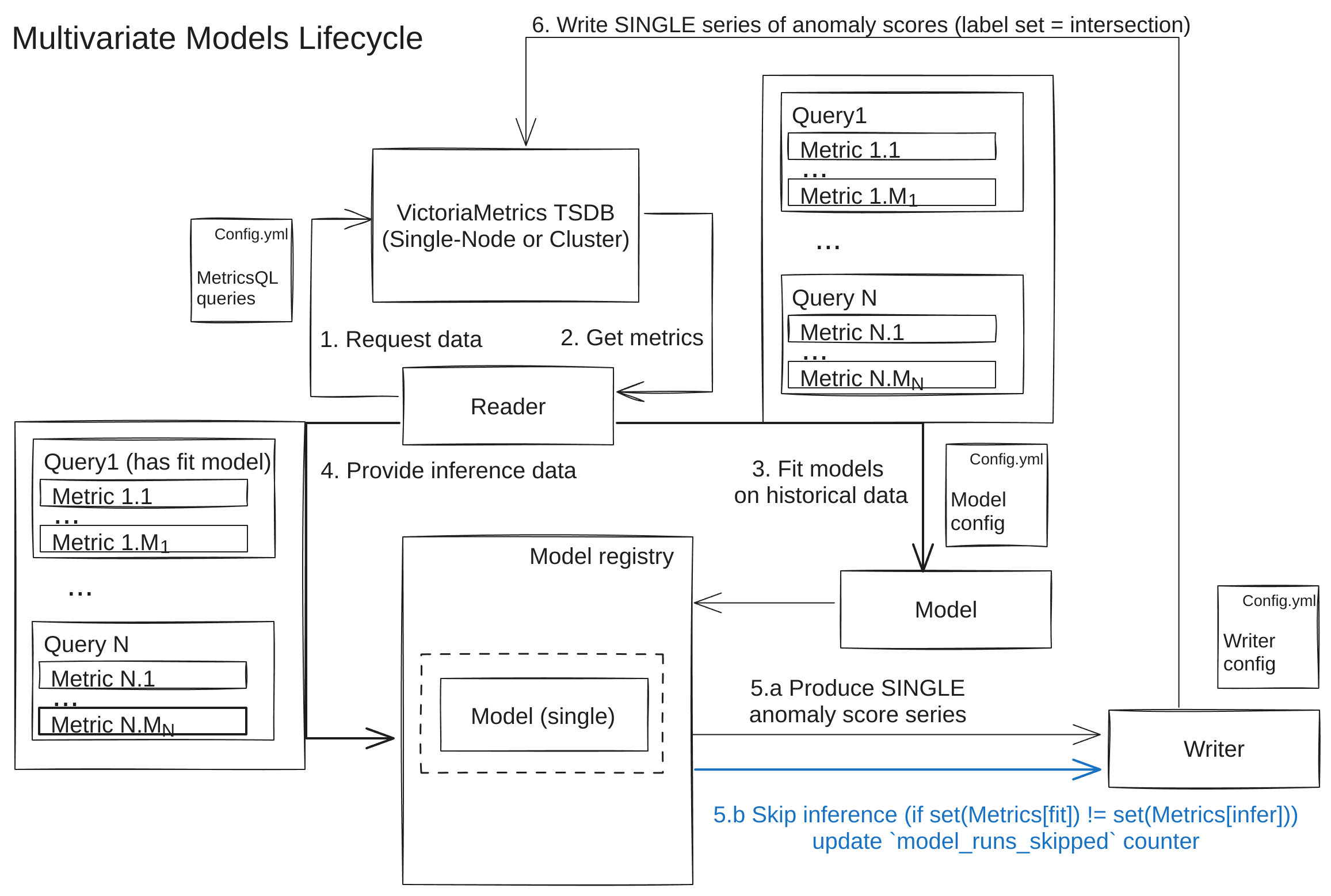

Multivariate Models

For a multivariate type, one shared model is fit/used for inference on all time series simultaneously, defined in its queries arg.

For example, if you have some multivariate model to use 3 MetricQL queries, each returning 5 time series, there will be one shared model created in total. Once fit, this model will expect exactly 15 time series with exact same labelsets as an input. This model will produce one shared output.

If during an inference, you got a different amount of series or some series having a new labelset (not present in any of fitted models), the inference will be skipped until you get a model, trained particularly for such labelset during forthcoming re-fit step.

Implications: Multivariate models are a go-to default, when your queries returns fixed amount of individual time series (say, some aggregations), to be used for adding cross-series (and cross-query) context, useful for catching collective anomalies or novelties (expanded to multi-input scenario). For example, you may set it up for anomaly detection of CPU usage in different modes (idle, user, system, etc.) and use its cross-dependencies to detect unseen (in fit data) behavior.

Examples: IsolationForest

Rolling Models

A rolling model is a model that, once trained, cannot be (naturally) used to make inference on data, not seen during its fit phase.

An instance of rolling model is simultaneously fit and used for inference during its infer method call.

As a result, such model instances are not stored between consecutive re-fit calls (defined by fit_every arg in PeriodicScheduler), leading to lower RAM consumption.

Such models put more pressure on your reader's source, i.e. if your model should be fit on large amount of data (say, 14 days with 1-minute resolution) and at the same time you have frequent inference (say, once per minute) on new chunks of data - that's because such models require (fit + infer) window of data to be fit first to be used later in each inference call.

Note

: Rolling models require

fit_everyeither to be missing or explicitly set equal toinfer_everyin your PeriodicScheduler.

Examples: RollingQuantile

Non-Rolling Models

Everything that is not classified as rolling.

Produced models can be explicitly used to infer on data, not seen during its fit phase, thus, it doesn't require re-fit procedure.

Such models put less pressure on your reader's source, i.e. if you fit on large amount of data (say, 14 days with 1-minute resolution) but do it occasionally (say, once per day), at the same time you have frequent inference(say, once per minute) on new chunks of data

Note

: However, it's still highly recommended, to keep your model up-to-date with tendencies found in your data as it evolves in time.

Produced model instances are stored in-memory between consecutive re-fit calls (defined by fit_every arg in PeriodicScheduler), leading to higher RAM consumption.

Examples: Prophet

Online Models

Introduced in v1.15.0, online (incremental) models allow defining a smaller frame fit_window and less frequent fit calls to reduce the data burden from VictoriaMetrics. They make incremental updates to model parameters during each infer_every call, even on a single datapoint.

If the model doesn't support online mode, it's called offline (its parameters are only updated during fit calls).

Main differences between offline and online:

Fit stage

- Both types have a

fitstage, run on thefit_windowdata frame. - For offline models,

fit_windowshould contain enough data to train the model (e.g., 2 seasonal periods). - For online models, training can start gradually from smaller chunks (e.g., 1 hour).

Infer stage

- Both types have an

inferstage, run on new datapoints (timestamps > last seen timestamp of the previousinfercall). - Offline models use a pre-trained (during

fitcall) static model to make everyinfercall until the nextfitcall, when the model is completely re-trained. - Online models use a pre-trained (during

fitcall) dynamic model, which is gradually updated during eachinfercall with new datapoints. However, to prevent the model from accumulating outdated behavior, eachfitcall resets the model from scratch.

Strengths:

- The ability to distribute the data load evenly between the initial

fitand subsequentinfercalls. For example, an online model can be fit on 101mdatapoints during the initialfitstage once per month and then be gradually updated on the same 101mdatapoints during eachinfercall each 10 minutes. - The model can adapt to new data patterns (gradually updating itself during each

infercall) without needing to wait for the nextfitcall and one big re-training. - Slightly faster training/updating times compared to similar offline models.

Limitations:

- Until the online model sees enough data (especially if the data shows strong seasonality), its predictions might be unstable, producing more false positives (

anomaly_score > 1) or making false negative predictions, skipping real anomalies. - Not all models (e.g., complex ones like Prophet) have a direct online alternative, thus their applicability can be somewhat limited.

Each of the (built-in or custom) online models (like OnlineZscoreModel) shares the following common parameters and properties:

n_samples_seen_(int) - this model property refers to the number of datapoints the model was trained on and increases from 0 (before the firstfit) with each consecutiveinfercall.min_n_samples_seen(int), optional - this parameter defines the minimum number of samples to be seen before reliably computing the anomaly score. Otherwise, the anomaly score will be 0 untiln_samples_seen_>min_n_samples_seen, as there is not enough data to trust the model's predictions. For example, if your data has hourly seasonality and '1m' frequency, settingmin_n_samples_seen_to 288 (1440 minutes in a day / 5 minutes) should be sufficient.

Offline models

Every other model that isn't online. Offline models are completely re-trained during fit call and aren't updated during consecutive infer calls.

Built-in Models

Overview

VictoriaMetrics Anomaly Detection models support 2 groups of parameters:

vmanomaly-specific arguments - please refer to Parameters specific for vmanomaly and Default model parameters subsections for each of the models below.- Arguments to inner model (say, Facebook's Prophet), passed in a

argsargument as key-value pairs, that will be directly given to the model during initialization to allow granular control. Optional.

Note

: For users who may not be familiar with Python data types such as

list[dict], a dictionary in Python is a data structure that stores data values in key-value pairs. This structure allows for efficient data retrieval and management.

Models:

- AutoTuned - designed to take the cognitive load off the user, allowing any of built-in models below to be re-tuned for best params on data seen during each

fitphase of the algorithm. Tradeoff is between increased computational time and optimized results / simpler maintenance. - Prophet - the most versatile one for production usage, especially for complex data (trends, change points, multi-seasonality)

- Z-score - useful for initial testing and for simpler data (de-trended data without strict seasonality and with anomalies of similar magnitude as your "normal" data)

- Online Z-score - online alternative to Z-score model with exact same behavior and use cases.

- Holt-Winters - well-suited for data with moderate complexity, exhibiting distinct trends and/or single seasonal pattern.

- MAD (Median Absolute Deviation) - similarly to Z-score, is effective for identifying outliers in relatively consistent data (useful for detecting sudden, stark deviations from the median).

- Online MAD - approximate online alternative to MAD model, appropriate for the same use cases.

- Rolling Quantile - best for data with evolving patterns, as it adapts to changes over a rolling window.

- Online Seasonal Quantile - best used on de-trended data with strong (possibly multiple) seasonalities. Can act as a (slightly less powerful) online replacement to

ProphetModel. - Seasonal Trend Decomposition - similarly to Holt-Winters, is best for data with pronounced seasonal and trend components

- Isolation forest (Multivariate) - useful for metrics data interaction (several queries/metrics -> single anomaly score) and efficient in detecting anomalies in high-dimensional datasets

- Custom model - benefit from your own models and expertise to better support your unique use case.

AutoTuned

Tuning hyperparameters of a model can be tricky and often requires in-depth knowledge of Machine Learning. AutoTunedModel is designed specifically to take the cognitive load off the user - specify as little as anomaly_percentage param from (0, 0.5) interval and tuned_model_class (i.e. model.zscore.ZscoreModel) to get it working with best settings that match your data.

Parameters specific for vmanomaly:

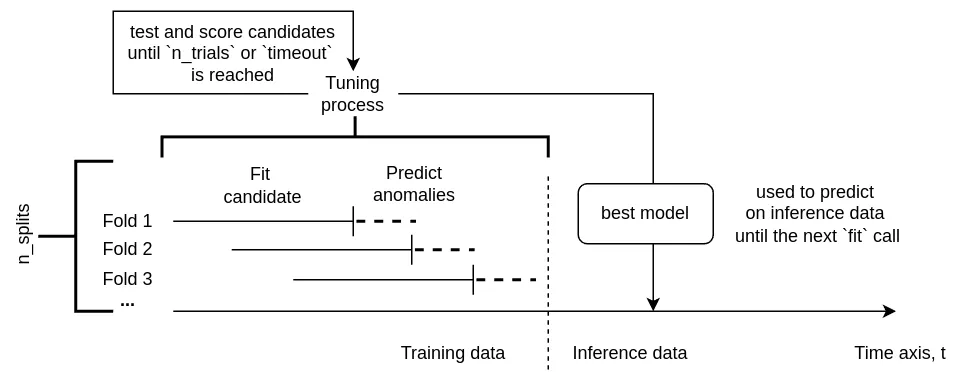

class(string) - model class name"model.auto.AutoTunedModel"(orautostarting from v1.13.0 with class alias support)tuned_class_name(string) - Built-in model class to tune, i.e.model.zscore.ZscoreModel(orzscorestarting from v1.13.0 with class alias support).optimization_params(dict) - Optimization parameters for unsupervised model tuning. Control % of found anomalies, as well as a tradeoff between time spent and the accuracy. The moretimeoutandn_trialsare, the better model configuration can be found fortuned_class_name, but the longer it takes and vice versa. Setn_jobsto-1to use all the CPUs available, it makes sense if only you have a big dataset to train on duringfitcalls, otherwise overhead isn't worth it.anomaly_percentage(float) - Expected percentage of anomalies that can be seen in training data, from (0, 0.5) interval.optimized_business_params(list[string]) - Starting from v1.15.0 this argument allows particular business-specific parameters such asdetection_directionormin_dev_from_expectedto remain unchanged during optimizations, retaining their default values. I.e. settingoptimized_business_paramsto['detection_direction']will allow to optimize onlydetection_directionbusiness-specific arg, whilemin_dev_from_expectedwill retain its default value (0.0). By default and if not set, will be equal to[](empty list), meaning no business params will be optimized. A recommended option is to leave it empty for more stable results and increased convergence (less iterations needed for a good result).seed(int) - Random seed for reproducibility and deterministic nature of underlying optimizations.n_splits(int) - How many folds to create for hyperparameter tuning out of your data. The higher, the longer it takes but the better the results can be. Defaults to 3.n_trials(int) - How many trials to sample from hyperparameter search space. The higher, the longer it takes but the better the results can be. Defaults to 128.timeout(float) - How many seconds in total can be spent on each model to tune hyperparameters. The higher, the longer it takes, allowing to test more trials out of definedn_trials, but the better the results can be.

# ...

models:

your_desired_alias_for_a_model:

class: 'auto' # or 'model.auto.AutoTunedModel' until v1.13.0

tuned_class_name: 'zscore' # or 'model.zscore.ZscoreModel' until v1.13.0

optimization_params:

anomaly_percentage: 0.004 # required. i.e. we expect <= 0.4% of anomalies to be present in training data

seed: 42 # fix reproducibility & determinism

n_splits: 4 # how much folds are created for internal cross-validation

n_trials: 128 # how many configurations to sample from search space during optimization

timeout: 10 # how many seconds to spend on optimization for each trained model during `fit` phase call

n_jobs: 1 # how many jobs in parallel to launch. Consider making it > 1 only if you have fit window containing > 10000 datapoints for each series

optimized_business_params: [] # business-specific params to include in optimization, if not set is empty list

# ...

Note

: There are some expected limitations of Autotune mode:

- It can't be made on your custom model.

- It can't be applied to itself (like

tuned_class_name: 'model.auto.AutoTunedModel')AutoTunedModelcan't be used on rolling models likeRollingQuantilein combination with on-disk model storage mode, as the rolling models exists only duringinfercalls and aren't persisted neither in RAM, nor on disk.

Prophet

Here we utilize the Facebook Prophet implementation, as detailed in their library documentation. All parameters from this library are compatible and can be passed to the model.

Note

:

ProphetModelis univariate, non-rolling, offline model.

Parameters specific for vmanomaly:

class(string) - model class name"model.prophet.ProphetModel"(orprophetstarting from v1.13.0 with class alias support)seasonalities(list[dict], optional) - Extra seasonalities to pass to Prophet. Seeadd_seasonality()Prophet param.

Note: Apart from standard vmanomaly output, Prophet model can provide additional metrics.

Additional output metrics produced by FB Prophet

Depending on chosen seasonality parameter FB Prophet can return additional metrics such as:

trend,trend_lower,trend_upperadditive_terms,additive_terms_lower,additive_terms_upper,multiplicative_terms,multiplicative_terms_lower,multiplicative_terms_upper,daily,daily_lower,daily_upper,hourly,hourly_lower,hourly_upper,holidays,holidays_lower,holidays_upper,- and a number of columns for each holiday if

holidaysparam is set

Config Example

models:

your_desired_alias_for_a_model:

class: 'prophet' # or 'model.prophet.ProphetModel' until v1.13.0

provide_series: ['anomaly_score', 'yhat', 'yhat_lower', 'yhat_upper', 'trend']

seasonalities:

- name: 'hourly'

period: 0.04166666666

fourier_order: 30

# Inner model args (key-value pairs) accepted by

# https://facebook.github.io/prophet/docs/quick_start.html#python-api

args:

# See https://facebook.github.io/prophet/docs/uncertainty_intervals.html

interval_width: 0.98

country_holidays: 'US'

Resulting metrics of the model are described here

Z-score

Note

:

ZScoreModelis univariate, non-rolling, offline model.

Model is useful for initial testing and for simpler data (de-trended data without strict seasonality and with anomalies of similar magnitude as your "normal" data).

Parameters specific for vmanomaly:

class(string) - model class name"model.zscore.ZscoreModel"(orzscorestarting from v1.13.0 with class alias support)z_threshold(float, optional) - standard score for calculation boundaries and anomaly score. Defaults to2.5.

Config Example

models:

your_desired_alias_for_a_model:

class: "zscore" # or 'model.zscore.ZscoreModel' until v1.13.0

z_threshold: 3.5

Resulting metrics of the model are described here.

Online Z-score

Note

:

OnlineZScoreModelis univariate, non-rolling, online model.

Online version of existing Z-score implementation with the same exact behavior and implications. Introduced in v1.15.0

Parameters specific for vmanomaly:

class(string) - model class name"model.online.OnlineZscoreModel"(orzscore_onlinestarting from v1.15.0 with class alias support)z_threshold(float, optional) - standard score for calculation boundaries and anomaly score. Defaults to2.5.min_n_samples_seen(int, optional) - the minimum number of samples to be seen (n_samples_seen_property) before computing the anomaly score. Otherwise, the anomaly score will be 0, as there is not enough data to trust the model's predictions. Defaults to 16.

Config Example

models:

your_desired_alias_for_a_model:

class: "zscore_online" # or 'model.online.OnlineZscoreModel'

z_threshold: 3.5

min_n_samples_seen: 128 # i.e. calculate it as full seasonality / data freq

provide_series: ['anomaly_score', 'yhat'] # common arg example

Resulting metrics of the model are described here.

Holt-Winters

Note

:

HoltWintersis univariate, non-rolling, offline model.

Here we use Holt-Winters Exponential Smoothing implementation from statsmodels library. All parameters from this library can be passed to the model.

Parameters specific for vmanomaly:

-

class(string) - model class name"model.holtwinters.HoltWinters"(orholtwintersstarting from v1.13.0 with class alias support) -

frequency(string) - Must be set equal to sampling_period. Model needs to know expected data-points frequency (e.g. '10m'). If omitted, frequency is guessed during fitting as the median of intervals between fitting data timestamps. During inference, if incoming data doesn't have the same frequency, then it will be interpolated. E.g. data comes at 15 seconds resolution, and our resample_freq is '1m'. Then fitting data will be downsampled to '1m' and internal model is trained at '1m' intervals. So, during inference, prediction data would be produced at '1m' intervals, but interpolated to "15s" to match with expected output, as output data must have the same timestamps. As accepted by pandas.Timedelta (e.g. '5m'). -

seasonality(string, optional) - As accepted by pandas.Timedelta. -

If

seasonal_periodsis not specified, it is calculated asseasonality/frequencyUsed to compute "seasonal_periods" param for the model (e.g. '1D' or '1W'). -

z_threshold(float, optional) - standard score for calculating boundaries to define anomaly score. Defaults to 2.5.

Default model parameters:

-

If parameter

seasonalis not specified, default value will beadd. -

If parameter

initialization_methodis not specified, default value will beestimated. -

args(dict, optional) - Inner model args (key-value pairs). See accepted params in model documentation. Defaults to empty (not provided). Example: {"seasonal": "add", "initialization_method": "estimated"}

Config Example

models:

your_desired_alias_for_a_model:

class: "holtwinters" # or 'model.holtwinters.HoltWinters' until v1.13.0

seasonality: '1d'

frequency: '1h'

# Inner model args (key-value pairs) accepted by statsmodels.tsa.holtwinters.ExponentialSmoothing

args:

seasonal: 'add'

initialization_method: 'estimated'

Resulting metrics of the model are described here.

MAD (Median Absolute Deviation)

Note

:

MADModelis univariate, non-rolling, offline model.

The MAD model is a robust method for anomaly detection that is less sensitive to outliers in data compared to standard deviation-based models. It considers a point as an anomaly if the absolute deviation from the median is significantly large.

Parameters specific for vmanomaly:

class(string) - model class name"model.mad.MADModel"(ormadstarting from v1.13.0 with class alias support)threshold(float, optional) - The threshold multiplier for the MAD to determine anomalies. Defaults to2.5. Higher values will identify fewer points as anomalies.

Config Example

models:

your_desired_alias_for_a_model:

class: "mad" # or 'model.mad.MADModel' until v1.13.0

threshold: 2.5

Resulting metrics of the model are described here.

Online MAD

Note

:

OnlineMADModelis univariate, non-rolling, online model.

The MAD model is a robust method for anomaly detection that is less sensitive to outliers in data compared to standard deviation-based models. It considers a point as an anomaly if the absolute deviation from the median is significantly large. This is the online approximate version, based on t-digests for online quantile estimation. introduced in v1.15.0

Parameters specific for vmanomaly:

class(string) - model class name"model.online.OnlineMADModel"(ormad_onlinestarting from v1.13.0 with class alias support)threshold(float, optional) - The threshold multiplier for the MAD to determine anomalies. Defaults to2.5. Higher values will identify fewer points as anomalies.min_n_samples_seen(int, optional) - the minimum number of samples to be seen (n_samples_seen_property) before computing the anomaly score. Otherwise, the anomaly score will be 0, as there is not enough data to trust the model's predictions. Defaults to 16.compression(int, optional) - the compression parameter for underlying t-digest. Higher values mean higher accuracy but higher memory usage. By default 100.

Config Example

models:

your_desired_alias_for_a_model:

class: "mad_online" # or 'model.online.OnlineMADModel'

threshold: 2.5

min_n_samples_seen: 128 # i.e. calculate it as full seasonality / data freq

compression: 100 # higher values mean higher accuracy but higher memory usage

provide_series: ['anomaly_score', 'yhat'] # common arg example

Resulting metrics of the model are described here.

Rolling Quantile

Note

:

RollingQuantileModelis univariate, rolling, offline model.

This model is best used on data with short evolving patterns (i.e. 10-100 datapoints of particular frequency), as it adapts to changes over a rolling window.

Parameters specific for vmanomaly:

class(string) - model class name"model.rolling_quantile.RollingQuantileModel"(orrolling_quantilestarting from v1.13.0 with class alias support)quantile(float) - quantile value, from 0.5 to 1.0. This constraint is implied by 2-sided confidence interval.window_steps(integer) - size of the moving window. (see 'sampling_period')

Config Example

models:

your_desired_alias_for_a_model:

class: "rolling_quantile" # or 'model.rolling_quantile.RollingQuantileModel' until v1.13.0

quantile: 0.9

window_steps: 96

Resulting metrics of the model are described here.

Online Seasonal Quantile

Note

:

OnlineSeasonalQuantileis univariate, non-rolling, online model.

Online (seasonal) quantile utilizes a set of approximate distributions, based on t-digests for online quantile estimation. Introduced in v1.15.0.

Best used on de-trended data with strong (possibly multiple) seasonalities. Can act as a (slightly less powerful) replacement to ProphetModel.

It uses the quantiles triplet to calculate yhat_lower, yhat, and yhat_upper output, respectively, for each of the min_subseasons sub-intervals contained in seasonal_interval. For example, with '4d' + '2h' seasonality patterns (multiple), it will hold and update 24*4 / 2 = 48 consecutive estimates (each 2 hours long).

Parameters specific for vmanomaly:

class(string) - model class name"model.online.OnlineSeasonalQuantile"(orquantile_onlinestarting from v1.13.0 with class alias support)quantiles(list[float], optional) - The quantiles to estimate.yhat_lower,yhat,yhat_upperare the quantile order. By default (0.01, 0.5, 0.99).seasonal_interval(string, optional) - the interval for the seasonal adjustment. If not set, the model will equal to a simple online quantile model. By default not set.min_subseason(str, optional) - the minimum interval to estimate quantiles for. By default not set. Note that the minimum interval should be a multiple of the seasonal interval, i.e. if seasonal_interval='2h', then min_subseason='15m' is valid, but '37m' is not.use_transform(bool, optional) - whether to internally apply alog1p(abs(x)) * sign(x)transformation to the data to stabilize internal quantile estimation. Does not affect the scale of produced output (i.e.yhat) By default False.global_smoothing(float, optional) - the smoothing parameter for the global quantiles. i.e. the output is a weighted average of the global and seasonal quantiles (ifseasonal_intervalandmin_subseasonargs are set). Should be from[0, 1]interval, where 0 means no smoothing and 1 means using only global quantile values.scale(float, optional) - the scaling factor for theyhat_lowerandyhat_upperquantiles. By default 1.0 (no scaling). if > 1, increases the boundaries [yhat_lower,yhat_upper] that define "non-anomalous" points. Should be > 0.season_starts_from(str, optional) - the start date for the seasonal adjustment, as a reference point to start counting the intervals. By default '1970-01-01'.min_n_samples_seen(int, optional) - the minimum number of samples to be seen (n_samples_seen_property) before computing the anomaly score. Otherwise, the anomaly score will be 0, as there is not enough data to trust the model's predictions. Defaults to 16.compression(int, optional) - the compression parameter for the underlying t-digests. Higher values mean higher accuracy but higher memory usage. By default 100.

Config Example

Suppose we have a data with strong intraday (hourly) and intraweek (daily) seasonality, data granularity is '5m' with up to 5% expected outliers present in data. Then you can apply similar config:

models:

your_desired_alias_for_a_model:

class: "quantile_online" # or 'model.online.OnlineSeasonalQuantile'

quantiles: [0.025, 0.5, 0.975] # lowered to exclude anomalous edges, can be compensated by `scale` param > 1

seasonal_interval: '7d' # longest seasonality (week, day) = week, starting from `season_starts_from`

min_subseason: '1h' # smallest seasonality (week, day, hour) = hour, will have its own quantile estimates

min_n_samples_seen: 288 # 1440 / 5 - at least 1 full day, ideal = 1440 / 5 * 7 - one full week (seasonal_interval)

scale: 1.1 # to compensate lowered quantile boundaries with wider intervals

season_starts_from: '2024-01-01' # interval calculation starting point, expecially for uncommon seasonalities like '36h' or '12d'

compression: 100 # higher values mean higher accuracy but higher memory usage

provide_series: ['anomaly_score', 'yhat'] # common arg example

Resulting metrics of the model are described here.

Seasonal Trend Decomposition

Note

:

StdModelis univariate, rolling, offline model.

Here we use Seasonal Decompose implementation from statsmodels library. Parameters from this library can be passed to the model. Some parameters are specifically predefined in vmanomaly and can't be changed by user(model='additive', two_sided=False).

Parameters specific for vmanomaly:

class(string) - model class name"model.std.StdModel"(orstdstarting from v1.13.0 with class alias support)period(integer) - Number of datapoints in one season.z_threshold(float, optional) - standard score for calculating boundaries to define anomaly score. Defaults to2.5.

Config Example

models:

your_desired_alias_for_a_model:

class: "std" # or 'model.std.StdModel' starting from v1.13.0

period: 2

Resulting metrics of the model are described here.

Additional output metrics produced by Seasonal Trend Decomposition model

resid- The residual component of the data series.trend- The trend component of the data series.seasonal- The seasonal component of the data series.

Isolation forest (Multivariate)

Note

:

IsolationForestModelis univariate, non-rolling, offline model.

Note

:

IsolationForestMultivariateModelis multivariate, non-rolling, offline model.

Detects anomalies using binary trees. The algorithm has a linear time complexity and a low memory requirement, which works well with high-volume data. It can be used on both univariate and multivariate data, but it is more effective in multivariate case.

Important: Be aware of the curse of dimensionality. Don't use single multivariate model if you expect your queries to return many time series of less datapoints that the number of metrics. In such case it is hard for a model to learn meaningful dependencies from too sparse data hypercube.

Here we use Isolation Forest implementation from scikit-learn library. All parameters from this library can be passed to the model.

Parameters specific for vmanomaly:

-

class(string) - model class name"model.isolation_forest.IsolationForestMultivariateModel"(orisolation_forest_multivariatestarting from v1.13.0 with class alias support) -

contamination(float or string, optional) - The amount of contamination of the data set, i.e. the proportion of outliers in the data set. Used when fitting to define the threshold on the scores of the samples. Default value - "auto". Should be either"auto"or be in the range (0.0, 0.5]. -

seasonal_features(list of string) - List of seasonality to encode through cyclical encoding, i.e.dow(day of week). Introduced in 1.12.0.- Empty by default for backward compatibility.

- Example:

seasonal_features: ['dow', 'hod']. - Supported seasonalities:

- "minute" - minute of hour (0-59)

- "hod" - hour of day (0-23)

- "dow" - day of week (1-7)

- "month" - month of year (1-12)

-

args(dict, optional) - Inner model args (key-value pairs). See accepted params in model documentation. Defaults to empty (not provided). Example: {"random_state": 42, "n_estimators": 100}

Config Example

models:

your_desired_alias_for_a_model:

# To use univariate model, substitute class argument with "model.isolation_forest.IsolationForestModel".

class: "isolation_forest_multivariate" # or 'model.isolation_forest.IsolationForestMultivariateModel' until v1.13.0

contamination: "0.01"

provide_series: ['anomaly_score']

seasonal_features: ['dow', 'hod']

args:

n_estimators: 100

# i.e. to assure reproducibility of produced results each time model is fit on the same input

random_state: 42

Resulting metrics of the model are described here.

vmanomaly output

When vmanomaly is executed, it generates various metrics, the specifics of which depend on the model employed.

These metrics can be renamed in the writer's section.

The default metrics produced by vmanomaly include:

-

anomaly_score: This is the primary metric.- It is designed in such a way that values from 0.0 to 1.0 indicate non-anomalous data.

- A value greater than 1.0 is generally classified as an anomaly, although this threshold can be adjusted in the alerting configuration.

- The decision to set the changepoint at 1 was made to ensure consistency across various models and alerting configurations, such that a score above 1 consistently signifies an anomaly.

-

yhat: This represents the predicted expected value. -

yhat_lower: This indicates the predicted lower boundary. -

yhat_upper: This refers to the predicted upper boundary. -

y: This is the original value obtained from the query result.

Important: Be aware that if NaN (Not a Number) or Inf (Infinity) values are present in the input data during infer model calls, the model will produce NaN as the anomaly_score for these particular instances.

vmanomaly monitoring metrics

Each model exposes several monitoring metrics to its health_path endpoint:

Custom Model Guide

Apart from vmanomaly built-in models, users can create their own custom models for anomaly detection.

Here in this guide, we will

- Make a file containing our custom model definition

- Define VictoriaMetrics Anomaly Detection config file to use our custom model

- Run service

Note

: The file containing the model should be written in Python language (3.11+)

1. Custom model

Note

: By default, each custom model is created as univariate / non-rolling model. If you want to override this behavior, define models inherited from

RollingModel(to get a rolling model), or havingis_multivariateclass arg set toTrue(please refer to the code example below).

We'll create custom_model.py file with CustomModel class that will inherit from vmanomaly's Model base class.

In the CustomModel class, the following methods are required: - __init__, fit, infer, serialize and deserialize:

-

__init__method should initiate parameters for the model.Note: if your model relies on configs that have

argkey-value pair argument, like Prophet, do not forget to use Python's**kwargsin method's signature and to explicitly callsuper().__init__(**kwargs)to initialize the base class each model derives from

-

fitmethod should contain the model training process. Please be aware that forRollingModeldefiningfitmethod is not needed, as the whole fit/infer process should be defined completely ininfermethod. -

infershould return Pandas.DataFrame object with model's inferences. -

serializemethod that saves the model on disk. -

deserializeload the saved model from disk.

For the sake of simplicity, the model in this example will return one of two values of anomaly_score - 0 or 1 depending on input parameter percentage.

import numpy as np

import pandas as pd

import scipy.stats as st

import logging

from pickle import dumps

from model.model import (

PICKLE_PROTOCOL,

Model,

deserialize_basic

)

# from model.model import RollingModel # inherit from it for your model to be of rolling type

logger = logging.getLogger(__name__)

class CustomModel(Model):

"""

Custom model implementation.

"""

# by default, each `Model` will be created as a univariate one

# uncomment line below for it to be of multivariate type

# is_multivariate = True

# by default, each `Model` will be created as offline

# uncomment line below for it to be of type online

# is_online = True

def __init__(self, percentage: float = 0.95, **kwargs):

super().__init__(**kwargs)

self.percentage = percentage

self._mean = np.nan

self._std = np.nan

def fit(self, df: pd.DataFrame):

# Model fit process:

y = df['y']

self._mean = np.mean(y)

self._std = np.std(y)

if self._std == 0.0:

self._std = 1 / 65536

def infer(self, df: pd.DataFrame) -> np.array:

# Inference process:

y = df['y']

zscores = (y - self._mean) / self._std

anomaly_score_cdf = st.norm.cdf(np.abs(zscores))

df_pred = df[['timestamp', 'y']].copy()

df_pred['anomaly_score'] = anomaly_score_cdf > self.percentage

df_pred['anomaly_score'] = df_pred['anomaly_score'].astype('int32', errors='ignore')

return df_pred

def serialize(self) -> None:

return dumps(self, protocol=PICKLE_PROTOCOL)

@staticmethod

def deserialize(model: str | bytes) -> 'CustomModel':

return deserialize_basic(model)

2. Configuration file

Next, we need to create config.yaml file with vmanomaly configuration and model input parameters.

In the config file's models section we need to set our model class to model.custom.CustomModel (or custom starting from v1.13.0 with class alias support) and define all parameters used in __init__ method.

You can find out more about configuration parameters in vmanomaly config docs.

schedulers:

s1:

infer_every: "1m"

fit_every: "1m"

fit_window: "1d"

models:

custom_model:

class: "custom" # or 'model.model.CustomModel' until v1.13.0

percentage: 0.9

reader:

datasource_url: "http://victoriametrics:8428/"

sampling_period: '1m'

queries:

ingestion_rate: 'sum(rate(vm_rows_inserted_total)) by (type)'

churn_rate: 'sum(rate(vm_new_timeseries_created_total[5m]))'

writer:

datasource_url: "http://victoriametrics:8428/"

metric_format:

__name__: "custom_$VAR"

for: "$QUERY_KEY"

run: "test-format"

monitoring:

# /metrics server.

pull:

port: 8080

push:

url: "http://victoriametrics:8428/"

extra_labels:

job: "vmanomaly-develop"

config: "custom.yaml"

3. Running custom model

Let's pull the docker image for vmanomaly:

docker pull victoriametrics/vmanomaly:latest

Now we can run the docker container putting as volumes both config and model file:

Note

: place the model file to

/model/custom.pypath when copying

./custom_model.py:/vmanomaly/model/custom.py

docker run -it \

-v $(PWD)/license:/license \

-v $(PWD)/custom_model.py:/vmanomaly/model/custom.py \

-v $(PWD)/custom.yaml:/config.yaml \

victoriametrics/vmanomaly:latest /config.yaml \

--license-file=/license

Please find more detailed instructions (license, etc.) here

Output

As the result, this model will return metric with labels, configured previously in config.yaml.

In this particular example, 2 metrics will be produced. Also, there will be added other metrics from input query result.

{__name__="custom_anomaly_score", for="ingestion_rate", model_alias="custom_model", scheduler_alias="s1", run="test-format"},

{__name__="custom_anomaly_score", for="churn_rate", model_alias="custom_model", scheduler_alias="s1", run="test-format"}